11 The Omotokata (2): Consolidation of Profit

This is the record prepared twice yearly by the Omotokata, listing total assets and income and expenditures for Mitsui’s businesses. It is one of the most important historical documents relating to those businesses, making it possible to track changes in the capital, assets, and liabilities of the Omotokata, with fiscal reporting periods generally ending on lunar July 14 and December 31. The individual booklets are stored folded, in Japanese paper sleeves, and open out horizontally. They are in surprisingly good condition, demonstrating their importance as records of their time, and cover a period of roughly 160 years, from 1710 to 1873, with only a minor amount of content missing.

The Line Items of the Omotokata Kanjomokuroku

The Omotokata Kanjomokuroku was divided into three categories: (1) azukarikata (capital and liabilities) and kashikata (assets); (2) irikata (revenues) and haraikata (expenses); and (3) mototate sashihiki (the total of changes in the amount of assets and real estate). In addition, after total assets were calculated, (4) the respective claims of the 11 Mitsui families on those assets were calculated. The difference between the two totals, which was termed nobegin (current profit), matches and takes the form of double-entry bookkeeping. However, there were also differences with today’s bookkeeping, with items known today as “credit” and “debit” termed “deposit” and “credit” respectively. In addition, until the late 18th century, there were other practices that differed from modern bookkeeping, including recording some real estate in (3), separately from (1). (4) is based on the proportionate claim recorded in the Sochiku Isho (→09) and is one of the unique features of the Omotokata Kanjomokuroku. However, the portions of Mitsui’s total wealth that was nominally to the 11 families were not actually distributed.

The Structure of the Omotokata Kanjomokuroku

For example, for the year 1774, when total assets of the Omotokata reached their peak value in nominal terms, we see the following: (1), azukarikata, totaled 81,989 kan 796 monme in silver, including 2 kan 878 monme in silver and 15,024 ryo in gold as accumulated interest for loans to the daimyo of the Kishu domain. Kashikata totaled 82,063 kan 508 monme in silver, including loans to the Kyoto money exchange store of 56,094 ryo in gold and 258 kan in silver that was lent to daimyos. It also included significant amounts of impaired assets in the form of loans to daimyos. Subtracting kashikata from azukarikata results in 73 kan 711 monme in silver of deferred funds.

(2), irikata, totaled 538 kan 76 monme in silver, including 333 ryo in gold and 106 kan 660 monme in silver as remittances from each store, while haraikata totaled 464 kan 365 monme in silver, including living expenses for the Mitsui Domyo totaling 272 ryo in gold and 161 kan 578 monme in silver. Subtracting haraikata from irikata equals 73 kan 711 monme. The difference in (1) and the difference in (2) are the same.

(3), mototate sashihiki, is the total of the previous term’s assets of 50,025 kan 796 monme and the current term’s deferred funds of 73 kan 711 monme in silver. This, plus 8,372 kan 250 monme of real estate, amounts to total assets of 58,471 kan 758 monme in silver (approximately 980,000 ryo in gold at the rate of 1 ryo = 60 monme).

Settlement and Profit Accumulation

Mitsui’s business was divided into the kimono division and the financial division, with each Kyoto shop managing and operating its own division, supervised by the Omotokata. Settlement was effected by each shop’s submission of its accounting ledgers to its respective Kyoto kimono shop or money exchange store, which closed the accounts and in turn submitted them to the Omotokata. The latter prepared a final settlement of accounts by closing the accounts of the two divisions, including its own income and expenditure, and prepared the Omotokata Kanjomokuroku.

Each shop set aside its business profits for the Omotokata, and these profits would be remitted to the Omotokata at the end of the fiscal term. Prior to the second half of the 18th century, the Omotokata accumulated the total profits of each shop on a three-year fiscal term basis.

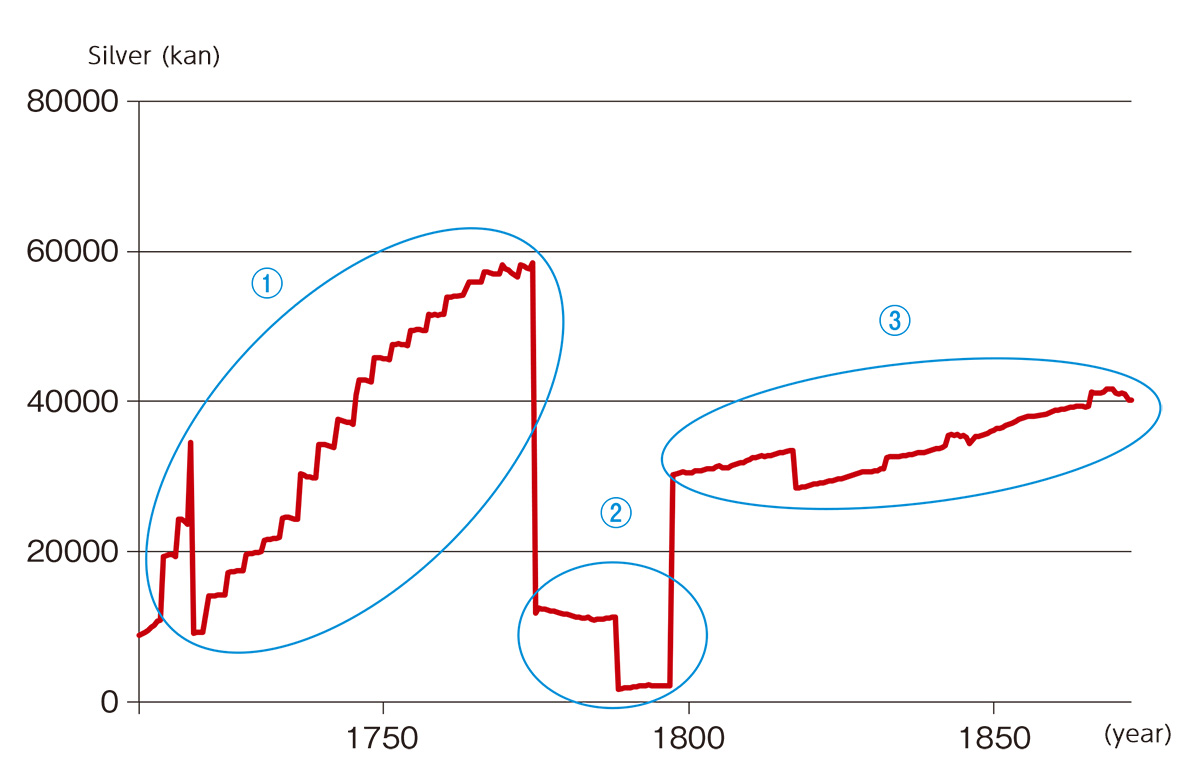

Assets Over Time

Total assets of the Omotokata from 1710 to 1872 (→Fig. 11b). Roughly speaking, there were three main periods.

(1) 1710 to 1774 The initial revenue surge is attributable to shop profits remitted to the Omotokata after its establishment. The switch from gold to silver in 1718 reduced the book value to less than half, but assets rose sawtooth-fashion thereafter. This was due to steady accumulation of profits by the kimono and financial divisions during the three-year fiscal terms. The peak was reached in 1774, as noted.

(2) 1774 to 1797 After the Anei Settlement (→10) divided Mitsui’s assets into three categories and liquidated non-performing loans, the Omotokata’s total assets shrank by roughly 80 percent. Remittances from the kimono and financial divisions decreased, and the three-year accounting period was also abandoned.

(3) 1797 to 1872 Following the Kansei Unification (→10), the assets of all businesses were once again gathered into the Omotokata. However, due to such factors as remittances from the businesses being set at a fixed amount, the Omotokata’s ability to oversee all assets of the business was greatly reduced. Total assets increased gradually until the late 19th century, but included many impaired assets. When significant liquidity was required, the Omotokata sometimes met the need by borrowing from the money exchange store.

From the 1800s on, loans from the Mitsui Domyo increased rapidly (→21), and the Omotokata struggled to pay its debts. In the latter half of the 19th century, Omotokata management was further complicated by mismanagement on the part of Hondana Ichimaki (→21)and the repeated imposition of extraordinary taxes by the Tokugawa government.